Did you know that almost 70% of people turning 65 today will need long-term care at some point in their lives? It’s a staggering statistic that often gets overlooked in retirement conversations. Addressing this challenge proactively can make a world of difference in financial stability and peace of mind.

Long-term care insurance originated in the 1980s as a safeguard against the rising costs of extended care. Today, it plays a crucial role in comprehensive retirement planning. With the average annual cost of a private room in a nursing home exceeding $100,000, having a solid plan in place is more important than ever.

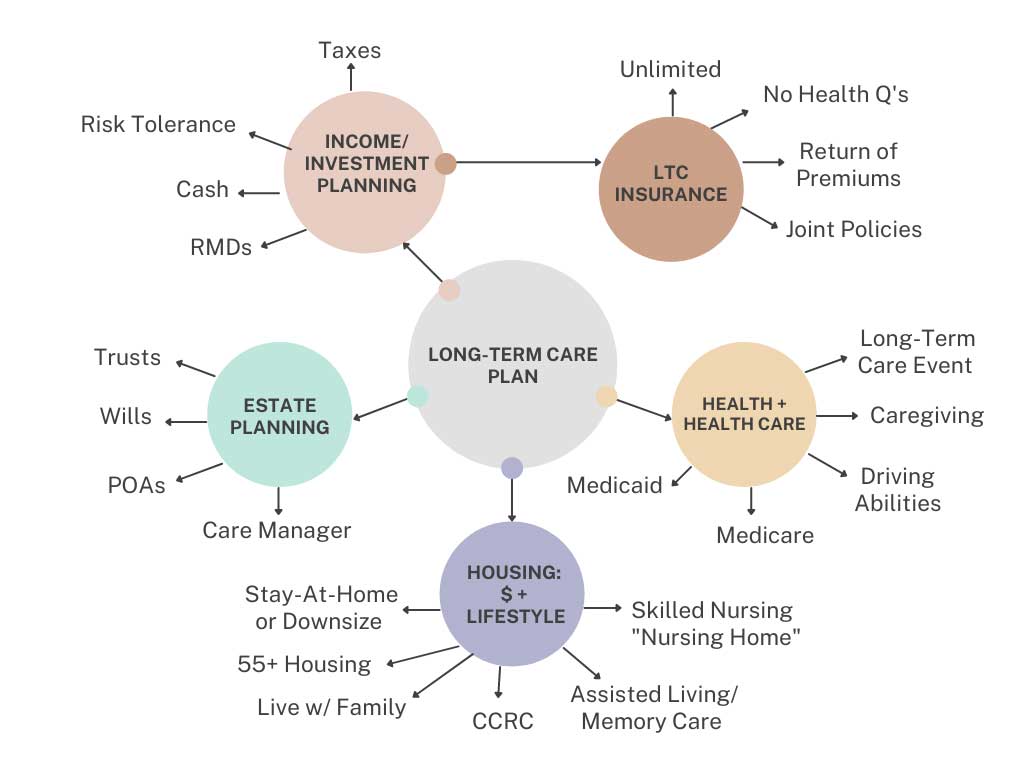

Understanding Longterm Care Insurance

Longterm care insurance is a type of policy designed to cover the costs of long-term care services. These services can include things like home care, nursing home stays, and assisted living. It’s an important part of financial planning for many people as they age.

The main goal of longterm care insurance is to help policyholders maintain their independence. By covering care costs, it reduces the financial burden on families. This coverage ensures that individuals receive the care they need without depleting their savings.

There are different types of longterm care insurance policies available. Some offer more comprehensive coverage, while others may be more affordable but provide fewer benefits. Choosing the right policy depends on individual needs and financial situations.

Many people may not realize that their health insurance or Medicare does not cover most long-term care services. That’s why longterm care insurance can be so valuable. It fills in the gaps, providing peace of mind for the future.

Does Your Retirement Plan Account For Long Term Care?

The Importance of Longterm Care Insurance in Retirement Planning

Longterm care insurance plays a crucial role in ensuring a secure and comfortable retirement. It provides a safety net by covering the expenses of extended care services, which can otherwise be a huge financial burden. This insurance helps protect your savings and assets, allowing you to enjoy your retirement without constant financial stress.

Financial Protection

One of the primary reasons for having longterm care insurance is financial protection. The cost of long-term care can be staggering, draining your retirement funds quickly. Having this insurance ensures your savings and investments are safeguarded.

This type of coverage can help avoid scenarios where you might have to sell assets to pay for care. By securing longterm care insurance, you are effectively planning for unforeseen financial challenges. It provides peace of mind, knowing that your finances are protected.

Additionally, it can cover services not included in standard health insurance or Medicare, filling significant gaps in coverage. This benefit ensures comprehensive care without depleting your resources. It’s a proactive step towards comprehensive retirement planning.

Ensuring Quality Care

Longterm care insurance ensures that you receive high-quality care when needed. Policies often cover services like skilled nursing care, occupational therapy, and personal assistance. This coverage allows for access to better care options, improving quality of life.

Without insurance, you might have limited choices for care providers. Longterm care insurance broadens your options, ensuring you get the best possible care services. It helps maintain your standard of living and dignity in the later years of life.

Moreover, it allows you to choose care settings, whether at home or in a facility. This flexibility is crucial for personal comfort and well-being. Having a choice makes a significant difference during challenging times.

Reducing Family Stress

Another important aspect is the reduction of stress on family members. Without longterm care insurance, loved ones might have to bear the emotional and financial burdens of caregiving. Insurance coverage alleviates this pressure, allowing families to focus on spending quality time together.

Many families face tough decisions when it comes to care options. Longterm care insurance provides clear solutions, reducing conflicts and uncertainties. It ensures that your family is not left with difficult choices or financial strain.

This kind of insurance also supports hiring professional caregivers, which can enhance the quality of care. It allows families to involve skilled professionals, ensuring the best care possible. Ultimately, it fosters a more supportive and less stressful environment for everyone involved.

Features of Longterm Care Insurance

Longterm care insurance offers several key features to help cover the costs of extended care. One major aspect is the variety of services it covers, including home care, assisted living, and nursing home care. This breadth of coverage ensures you receive the necessary assistance regardless of the setting.

Policy benefits can also be customized to fit your needs. You can choose benefit amounts, coverage periods, and inflation protection options. These customizations make the insurance flexible and tailored to individual requirements.

Another essential feature is the elimination period, which is the waiting period before benefits start. This period can vary from 30 to 90 days, during which you’ll need to cover costs yourself. Choosing a shorter elimination period can provide quicker financial relief.

Many policies offer optional riders for additional coverage. For example, you can add shared care benefits or non-forfeiture benefits. These riders can enhance your policy, offering more comprehensive protection for your future care needs.

How to choose the Right Longterm Care Insurance

Selecting the right longterm care insurance involves assessing your personal needs and financial situation. Start by evaluating the type of care you might need in the future. Consider factors like family health history and lifestyle.

Next, compare policy options from various insurers. Look at the types of services covered, benefit amounts, and coverage limits. Choosing a policy with flexible options is crucial.

Don’t forget to check the elimination period, which is the waiting time before your benefits kick in. A shorter elimination period might be more expensive, but it offers quicker access to funds. Balance cost with your need for immediate coverage.

Consider adding optional riders to your policy for enhanced benefits. These can include inflation protection or shared care options. These riders can provide extra security and peace of mind.

It’s essential to read the fine print and understand the policy details. Pay attention to any exclusions or limitations. Knowing these details can prevent unexpected issues down the line.

Consult a financial advisor for expert advice tailored to your situation. They can help navigate the complexities of longterm care insurance. Making an informed decision ensures your future care needs are met.

Case Studies of Effective Use of Longterm Care Insurance in Retirement Planning

Let’s explore how John, a retired teacher, benefited from his longterm care insurance policy. After suffering a stroke, John required extensive rehabilitation and home care. His insurance covered these expenses, preserving his savings and ensuring he received proper care.

In another instance, Mary and her husband Tom had a joint policy. When Tom developed Alzheimer’s, the insurance provided funds for a specialized care facility. This allowed Mary to focus on her well-being without financial strain.

Consider the case of Sara, who added inflation protection to her policy. When she needed assisted living ten years later, the increased benefit amount matched the rising costs of care. This feature ensured her coverage remained adequate over time.

Jack and his family also benefited significantly. They opted for a shared care rider, allowing both spouses to draw from the same pool of benefits. This flexibility helped them manage costs effectively when Jack needed extended care services.

Lastly, we have Rachel, who chose a policy with a short elimination period. She required immediate care after an accident, and her insurance provided quick financial support. This prevented a significant financial burden during a challenging time.

These real-life examples demonstrate the crucial role of longterm care insurance in retirement planning. Proper planning and selecting the right policy can make all the difference. It ensures financial stability and quality care for you and your loved ones.

Do I Really Need Long-Term Care Insurance?

Conclusion

Longterm care insurance is a vital component of comprehensive retirement planning. It provides financial protection, ensures high-quality care, and reduces stress on families. With the right policy, you can protect your savings and maintain your quality of life.

Choosing the right plan involves careful consideration of your needs and financial situation. Whether it’s the flexibility of riders or the assurance of inflation protection, these features offer valuable benefits. Incorporating longterm care insurance into your retirement plan is a wise and proactive step.